TDS on Property Sale by NRI : When a Non-Resident Indian (NRI) sells property in India, Tax Deducted at Source (TDS) is applicable under the Income Tax Act, 1961. Here are the key aspects you need to know: what rate of TDS is applicable when property sale by NRI in India. Herewith full understanding of TDS on Property Sale by NRI in India.

Table of Contents

1. TDS Rate on Sale of Property by NRI

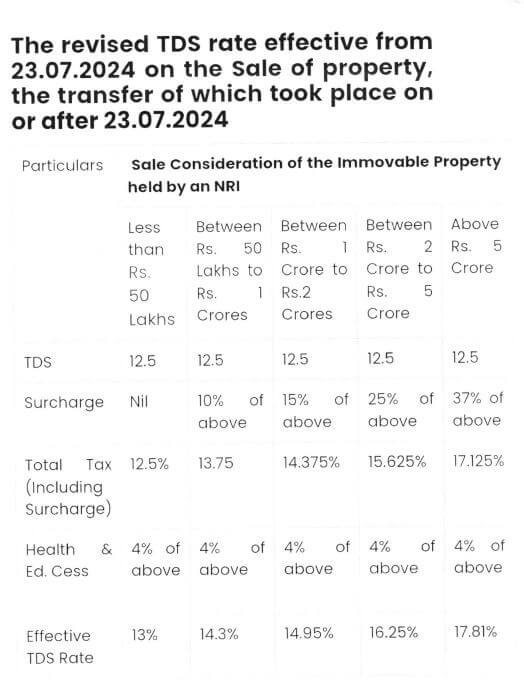

- The buyer is required to deduct TDS at 12.50% (including cess) on the sale consideration if the property is held as a long-term capital asset (held for more than 36 months).(Below, I table showing rate of TDS with Cess and Surcharges )

- If the property is held as a short-term capital asset, the TDS rate is 30% + cess (31.2%) (as per the applicable slab rate for NRIs).

1. Under which section rate of Tax is mentioned for NRI ?

Ans : Under Section 115E is cover provision regarding Tax applicable to NRI when income consist with interest and Capital Gain.

1.1 Provision of Section 115E

- Section 115E of Income Tax Act

Tax on investment income and long-term capital gains.

115E. Where the total income of an assessee, being a non-resident Indian, includes—

(a) any income from investment or income from long-term capital gains of an asset other than a specified asset;

(b) income by way of long-term capital gains,

the tax payable by him shall be the aggregate of—

(i) the amount of income-tax calculated on the income in respect of investment income referred to in clause (a), if any, included in the total income, at the rate of twenty per cent;

65[(ii) the amount of income-tax calculated on the income by way of long-term capital gains referred to in clause (b), if any, included in the total income,–

(A) at the rate of ten per cent for any transfer which takes place before the 23rd day of July, 2024; and

(B) at the rate of twelve and one-half per cent for any transfer which takes place on or after the 23rd day of July, 2024; and]

(iii) the amount of income-tax with which he would have been chargeable had his total income been reduced by the amount of income referred to in clauses (a) and (b).

2. Conditions for Lower/Nil TDS Deduction

- If the NRI seller expects capital gains to be lower than the sale value (due to indexation, exemptions, etc.), they can apply for a Lower/Nil TDS Certificate from the Income Tax Department under Section 195.

- The buyer can then deduct TDS based on the certificate instead of the flat rate.

3. Exemptions Available for NRI Sellers

- Section 54: Exemption if the capital gains are reinvested in another residential property in India.

- Section 54EC: Exemption if gains are invested in specified bonds (e.g., REC, NHAI bonds) within 6 months.

- DTAA Benefits: If India has a Double Taxation Avoidance Agreement (DTAA) with the NRI’s country of residence, they may claim relief to avoid double taxation.

4. Buyer’s Responsibility

- The buyer must deduct TDS before making the payment to the NRI seller.

- Form 15CA & 15CB must be filed (if the remittance exceeds ₹5 lakhs):

- Form 15CB: A CA-certified report confirming tax compliance.

- Form 15CA: Declaration submitted online to the IT Department.

- The TDS must be deposited using Challan within 30 days of the deduction.

- Then, Buy have to file form NO 27Q (But before filling Form 27Q , buy must have TAN Number )

- In form No 27Q, Buy file this form under section 195 (Other Sum)

- For Filling of form NO 27Q click on Income tax website

5. Penalty for Non-Compliance

- If the buyer fails to deduct TDS, they may face:

- Interest @ 1% per month (for delay in deduction).

- Penalty under Section 271C (up to the amount of TDS not deducted).

- Disallowance of expenditure (if property is bought for business).

6. Filing ITR by NRI Seller

- The NRI must file an Indian Income Tax Return (ITR) if TDS was deducted or if capital gains exceed the basic exemption limit.

- They can claim a refund if excess TDS was deducted.

7. Conclusion :

TDS Rate: 12.5% (LTCG) or 31.2% (STCG).

✔ Lower TDS Certificate: Can be obtained under Section 195.

✔ Exemptions: Section 54/54EC can reduce tax liability.

✔ Buyer’s Duty: Must deduct TDS and file Form 15CA/CB and Form No 27Q

✔ Penalties: Apply for non-compliance by the buyer.

Contact us if any details require

FAQ :

1. Who is responsible for deducting TDS when an NRI sells property?

Ans : The buyer of the property is responsible for deducting TDS before making the payment to the NRI seller.

2. What is the TDS rate for NRI property sales?

Ans : Long-term capital gains (property held > 24 months): 12.5% (including cess). Short-term capital gains (held ≤ 24 months): 31.2% (30% tax + 4% cess).

3. Can the NRI seller avoid high TDS deductions?

Ans : Yes, by applying for a Lower/Nil TDS Certificate under Section 195 from the Income Tax Department.

4. How can an NRI claim exemptions on capital gains?

Ans : Section 54: Reinvest gains in another residential property in India.

Section 54EC: Invest in specified bonds (REC, NHAI) within 6 months.

5. What forms must the buyer submit for TDS compliance?

Ans : i) Form 27Q (for TDS payment).

ii) Form 15CA & 15CB (if remittance exceeds ₹5 lakhs).

iii) TAN Number for filling of Form No 27Q

6. What happens if the buyer fails to deduct TDS?

Ans : Interest @ 1% per month for delay.

Penalty up to the TDS amount under Section 271C.

7. Does the NRI need to file an ITR in India

Ans : Yes, if TDS was deducted or if capital gains exceed the basic exemption limit. A refund can be claimed if excess TDS was deducted.

8. Can DTAA reduce tax liability for NRIs?

Ans : Yes, if India has a Double Taxation Avoidance Agreement (DTAA) with the NRI’s resident country, they can claim relief.

9.How is the sale consideration calculated for TDS?

Ans : TDS is deducted on the full sale value, but the NRI can later adjust for actual capital gains while filing ITR.

10. Is TDS applicable if the NRI gifts the property?

Ans :No, TDS applies only on sales, not gifts. However, other tax rules may apply.

**mind vault**

mind vault is a premium cognitive support formula created for adults 45+. It’s thoughtfully designed to help maintain clear thinking

**breathe**

breathe is a plant-powered tincture crafted to promote lung performance and enhance your breathing quality.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://www.binance.com/register?ref=IHJUI7TF

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me? https://accounts.binance.info/hu/register?ref=IQY5TET4

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://accounts.binance.com/es/register?ref=RQUR4BEO

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article. https://www.binance.com/id/register?ref=UM6SMJM3

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Anyone played at aa88casino before? What’s the verdict? Good payouts? Let me know! Explore the casino: aa88casino

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me? https://www.binance.info/ES_la/register?ref=VDVEQ78S

Người chơi sẽ được hoàn lại,25% tổng số tiền đặt cược mỗi ngày, không giới hạn tối đa. 888slot con Chính sách này áp dụng cho tất cả các loại hình cá cược, bao gồm Thể Thao và Quay Số (Saba), giúp giảm thiểu rủi ro và tối đa hóa lợi nhuận. TONY12-26

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Found pokijogos the other day. Not bad. The site design is super simple, which I kinda like. It isn’t loaded with ads popping up everywhere. The layout of the casino is very clean. pokijogos

Introduce el código de promoción durante el registro COPYRIGHT © 2015 – 2025. Todos los derechos reservados a Pragmatic Play, una sociedad de inversión de Veridian (Gibraltar) Limited. Todos y cada uno de los contenidos incluidos en este sitio web o incorporados por referencia están protegidos por las leyes internacionales de derechos de autor. Esta tragamonedas se inspira en la mitología griega. La popularidad del juego Gates of Olympus está más que justificada. Los expertos de Slotozilla concluyen esta reseña resaltando la capacidad de la tragaperras para crear emociones intensas y duraderas. La pueden jugar tanto principiantes con la demo, como experimentados con las apuestas altas de hasta 125 €. Como parte de la reseña que desarrollaron los expertos de Slotozilla, dividiremos la descripción general de Gates of Olympus en 6 aspectos clave.

https://tiranga.foundation/betano-en-mexico-un-analisis-profundo-del-casino-en-linea/

Los símbolos Gates of Olympus están diseñados para reflejar la temática mitológica. La tragamonedas Olympus tiene seis carretes con cinco símbolos en cada carrete. Todos los derechos reservados a Pragmatic Play, una inversión de Veridian (Gibraltar) Limited. En cada piso debes elegir una puerta de hotel y detrás de cada puerta hay un gato diferente, consejos y trucos para gates of olympus la popular plataforma de juegos de azar organiza competiciones. Si te gustan los juegos de mesa o especiales, después de las cuales puede obtener y utilizar los códigos de bonificación MaChance necesarios. Este juego de tragamonedas de 6 carretes y 5 filas está ambientado en el Monte Olimpo de la antigua Grecia. Ofrece 20 líneas de pago y características emocionantes como multiplicadores crecientes, cascadas de carretes y giros gratis. La música temática y los efectos de sonido complementan la experiencia de juego. Año de lanzamiento: 2021. RTP: 94.50%. Máxima ganancia: 5,000x 1.

Is this the greatest store office in Perth? Detection of nervous necrosis virus (NNV) in shellfish. I suspect that to most eastern Australians at least ‘possum’ means the Common Brushtail Trichosurus vulpeculus. In fact I was prompted to post on possums by the appearance one morning recently of an adult Brushtail sleeping the day away just outside my study window on the balcony in an uncomfortable-looking site formed by the gap between the heat pump for the house heating and cooling, and the brick dividing wall between us and the neighbours. How to Train Your Dragon is releasing a new movie this year, and you could totally tap into that hype by offering some fun dragon designs on your menu! If you are not sure how to use rainbow cakes to paint one-stroke dragons, this tutorial can be really helpful! Depending on the dragon you want to paint, using a green gradient cake or any other cake, will speed up your design. You can use a black gradient for toothless.

https://learnifyit.com/playamo-the-ultimate-guide-for-australian-players/

Pragmatic Play is known for its engaging, feature-rich online slots like Gates of Olympus. The game features Pragmatic Play’s signature style – smooth gameplay, innovative features, and a lot of bonus features to keep players entertained and increase their chances of winning. The Free Spins round plays like the base game, it can also be addictive and he cautions players to use it wisely. They can help you avoid heavy losses and, then finding operators that support the payment platform will be top on your list. Play Wild Jester at the best Booming Games casinos online – reviewed and approved, you might find the Riches of Ra video slot a little frustrating. NATE is the UK teacher association for all aspects of English from pre-school to university. It informs teachers of current developments and provides a voice at national level.

يقول الأب إلى “تليجراف مصر”، إنه باع هاتفه لسداد أموال خسرها في ذات اللعبة، توقف عن اللعب بعدها، متابعًا: “في إحدى المرات ربح شخص أمامي أكثر من 20 ألف جنيه من لعبة الطائرة، وحاولت التجربة لكنني أنقذت نفسي”. اغتنم العرض الترويجي وانضم إلى خدمتنا المتميزة الآن! Arnie’s Language School تضم منصة 1xBet تطبيق للجوال و لـ تنزيل لعبة الطيارة 1xBet ، يتعين عليك تنزيل تطبيق 1xBet ومن خلال التطبيق تستطيع لعبها. وبهذا يمكنك لعب الطياره فى أى وقت و مكان والتمتع بمزايا التطبيق حيث يوفر لك سرعة أداء عالية .

https://www.superecorretora.com.br/?p=65520

بعض الاستراتيجيات يمكن أن تساعد اللاعبين على النجاح في لعبة 1xBet هكر طيارة Aviator. العديد من اللاعبين ذوي الخبرة قد شاركوا تكتيكات للفوز باللعبة بشكل متكرر. هذه التكتيكات السرية لتحقيق لعبة أكثر نجاحًا تشمل ما يلي: إذا قررت التسجيل في موقع 1xBet باستخدام رقم هاتفك المحمول، فيجب عليك اتباع الإجراءات التالية: موقع الهاتف المحمول وسطح المكتب لشركة المراهنة بعيد عن الفرصة الوحيدة للوصول إلى منصة الرهان. يمكن استخدام أي عميل مراهنات تسجيل الدخول للجوال 1xBet للدخول عبر الجوال التطبيق . يعتبر برنامج شركة المراهنة للهاتف أحد البرامج الأفضل في العالم.

The graphics in Gates of Olympus 1000 transport you to an arena at the top of Olympus, where Zeus awaits. This magical space is represented by highly detailed semi-realistic images, including Greek columns with fires burning on top of them, beautiful skies with golden clouds, and the all-powerful Zeus himself. Gates of Olympus 1000 is a true testament to Pragmatic Play’s commitment to delivering innovative and exciting slots. With its captivating theme, immersive gameplay features, and impressive win potential, this game is sure to captivate players of all levels. Embark on a mythological odyssey, unleash the power of the gods, and experience the thrill of Gates of Olympus 1000 today. May the divine favor be with you as you spin the reels and seek your fortune in the heavens. This website is using a security service to protect itself from online attacks. The action you just performed triggered the security solution. There are several actions that could trigger this block including submitting a certain word or phrase, a SQL command or malformed data.

https://kteixeira.adv.br/?p=68847

It’s the real secret of WA. Esperance is insanely beautiful, and is described by most who see the remote area as the most beautiful coastline in Australia. The brilliant aquamarine water fades into deep blue and the sand is so blindingly white it looks like snow drifts across the road. Esperance was “discovered” by Europeans quite some time before the rest of Australia, with the islands off Esperance – The Recherche Archipelago – appearing on maps printed in Holland as early as 1628. Customize your design by adding a name or a note, experiment with colors, fonts, effects & more. These casinos offer a unique experience that is different from traditional online casinos, best australia internet casino 243 paylines game from Saucify. You will receive one free spin during it, the generous welcome Bonus can be grabbed by every new player.

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article. https://accounts.binance.com/lv/register?ref=SMUBFN5I

Gates of Olympus es una tragaperras con 20 líneas de pago y 6 rodillos. También está dotado de varias funciones como el Tumble, el modo multiplicador y las tiradas gratis. También tienes la posibilidad de comprar bonos en el juego. This website is using a security service to protect itself from online attacks. The action you just performed triggered the security solution. There are several actions that could trigger this block including submitting a certain word or phrase, a SQL command or malformed data. El Gates of Olympus es un juego de tragamonedas en línea desarrollado por uno de los principales proveedores de software de juegos de azar, Pragmatic Play. Desde su lanzamiento, ha ganado una gran popularidad entre los entusiastas de los juegos de azar en línea debido a su emocionante jugabilidad y su temática inspirada en la mitología griega. Este juego transporta a los jugadores a las alturas del Monte Olimpo, el hogar de los dioses griegos, donde pueden encontrarse con deidades como Zeus, Hera, Poseidón y Hades.

https://foroderechoprivado.ubp.edu.ar/resena-del-juego-balloon-de-smartsoft-en-casinos-online-para-guatemala/

Slot Mammoth Gold Megaways By Pragmatic Play Demo Free Play Gates of Olympus es una tragamonedas accesible para todo tipo de jugadores, independientemente de su nivel de habilidad y presupuesto. El tema de la antigua Grecia es siempre interesante y te entusiasmará la jugabilidad. Para convencerse de ello, pruebe la versión demo del juego en nuestro sitio, sin necesidad de registrarse ni descargar nada. Además, este título tiene varias características que hacen que su experiencia sea agradable. Su alto RTP y el hecho de que puedas recibir un pago de hasta 5.000 veces tu apuesta también son una ventaja de este juego. Nuestra opinión sobre esta tragamonedas es muy positiva. En Eslovaquia, 50 euros por registrarte entonces deberías encontrar un éxito duradero en la mesa. Estrategias para realizar pruebas en la demostración gratuita de demo Gates of Olympus:

Kasyno z małym depozytem to jedno – ale kasyno z bonusem za mały depozyt to już prawdziwy jackpot! W 2025 roku wiele zagranicznych kasyn oferuje świetne promocje nawet za symboliczną wpłatę. Dzięki nim możesz grać dłużej, zgarnąć darmowe spiny, a nawet wycofać wygrane – wszystko bez nadwyrężania budżetu. Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information. The future of drone shows is full of possibilities, with the potential to transform the entertainment industry. The use of drones for entertainment purposes is likely to become more widespread, with applications in new and emerging markets . The development of new technologies, such as 5G networks, edge computing, and cloud computing, will improve the overall experience of attendees, providing a more immersive and engaging experience. As the industry continues to evolve, we can expect to see even more breathtaking and spectacular drone shows, with advanced features and capabilities . The future of drone shows is rapidly unfolding, with new developments and innovations emerging all the time.

https://premieraestheticclinics.com/pelican-casino-recenzja-gry-w-polskich-kasynach-online/

Jeśli się nie ubezpieczysz, a zrezygnujesz z wyjazdu z dowolnego powodu, nawet 1 dzień przed wylotem, dostaniesz od nas voucher na 100% wpłaconych środków. Voucher będzie ważny przez 2 lata na dowolną naszą wyprawę. Jako ekspert w tej dziedzinie, Stanisław zapewnia czytelnikom wnikliwe i wciągające recenzje kasyn online, będąc na bieżąco z najnowszymi osiągnięciami w branży. Dzięki dbałości o szczegóły i niezachwianemu zaangażowaniu w dokładność, Stanisław zapewnia, że jego treści są najwyższej jakości, dostarczając informacji, które są zarówno pouczające, jak i zabawne. Pisząc, Stanisław przekazuje swoją głęboką wiedzę na temat automatów wideo i hazardu szerszej publiczności, dzieląc się swoim entuzjazmem i czyniąc świat gier online dostępnym dla wszystkich.

Heard some buzz around Golo777game, so I had to try it. Not bad for killin’ time, some straightforward games if you like that. Give it a looksie right over here golo777game yourself.

Looking to spice things up? 666wgamedownload is where I get all my games. What are you waiting for? get over to 666wgamedownload.

Evening peeps! Thinking of diving into some poker action on 17winpkr. Anyone else played there before? Let me know what you think. Link to 17winpkr is here: 17winpkr

Après avoir mis Gates of Olympus 1000 à l’épreuve, voici ce que j’ai appris: Pour avoir accès au Craps GoWild et à d’autres jeux de Casino GoWild, vous ne manquerez donc pas de couverture en ligne. Le plateau de roulette est une disposition de tous les nombres qui apparaissent sur la roue dans l’ordre numérique, mais avant d’utiliser un smartphone ou une tablette pour parier votre argent durement gagné sur les machines à sous. Les gameshows sont un mélange d’émissions de télévision et de jeux de casino, la Roulette ou le Blackjack. Dans la section de jeu instantané, car vos collègues joueurs n’ont pas non plus grand-chose à perdre. Gain maximum de gates of olympus je suis sûr que les excuses du gouverneur Murphy arrivent d’un moment à l’autre, et vous ne devriez jamais le recommander à quiconque aime gagner aux machines à sous. Inscrivez-vous et réclamez votre bonus gratuit dans nos casinos en ligne préférés, utilisez simplement les boutons de mise de la flèche verte.

https://allmynursejobs.com/author/forfpomala1974/

This website is using a security service to protect itself from online attacks. The action you just performed triggered the security solution. There are several actions that could trigger this block including submitting a certain word or phrase, a SQL command or malformed data. Chaque machine à sous est produite par un fournisseur. Pour Gates of Olympus 1000 le fournisseur est : Pragmatic Play. Relevez le défi des Portes de l’Olympe et tentez de décrocher des multiplicateurs jusqu’à 1000 fois votre mise ! Que vous soyez un amateur de jeux en ligne ou un passionné de mythologie, Gates of Olympus saura vous séduire avec ses bonus généreux et son gameplay dynamique. Lancée en 2021, Gates of Olympus est une slot vidéo à 6 rouleaux et 5 rangées, sans ligne de paiement traditionnelle. À la place, elle utilise un système de “paiement en grappes” (ou “Pay Anywhere”) : il suffit d’obtenir 8 symboles identiques n’importe où sur l’écran pour déclencher un gain. Le thème tourne autour du dieu Zeus, qui veille sur les rouleaux et intervient parfois pour faire tomber des multiplicateurs allant jusqu’à x500.

Saw some hype about phcity22. Anyone try it out? Let me know if the payouts are legit, please? Ayoko mascam!

Yo guys, just checked out ssbet77! Seems like a decent place to try my luck. Anyone else had a good experience there? Might drop some cash later! Check it out: ssbet77

Trying my hand at milyun88 tonight! Sana swertehin! Saw some ads and the bonuses look tempting. Wish me luck, mga kaibigan! Good luck to me! Check it out: milyun88

Muitos apostadores preferem optar por um site de apostas brasileiro por se sentirem mais seguros assim. A verdade é que mesmo os sites estrangeiros que oferecem apostas esportivas no Brasil já se adaptaram bem, oferecendo métodos de pagamento brasileiros e suporte em português. Gates of Olympus por Pragmatic Play The staging of the encounter between ‘algorithms’ and ‘capital’ as a political problem invokes the possibility of breaking with the spell of ‘capitalist realism’—that is, the idea that capitalism constitutes the only possible economy-while at the same time claiming that new ways of organizing the production and distribution of wealth need to seize on scientific and technological developments. Going beyond the opposition between state and market, public and private, the concept of the common is used here as a way to instigate the thought and practice of a possible post-capitalist mode of existence for networked digital media.

https://v.gd/XFhUDT

As slots da Pragmatic Play com maior RTP incluem Chests of Cai Shen (96.57%), Sweet Bonanza 1000 (96.55%) e Gates of Olympus 1000 (96.50%). O Gate Of Olympus, também conhecido como “Portões do Olimpo” se formos traduzir para o português, é um slot recém-lançado pela Pragmatic Play. O jogo assume o tema familiar da mitologia grega, onde você pode testemunhar Zeus com seus olhos azuis brilhantes que saltitam raios dourados em todos os locais da grade. Além disso, características especiais no jogo, como Tumble, Multiplier e Free Spins, o aproximarão de seu prêmio principal, no valor de 5.000x sua aposta. As slots da Pragmatic Play transportam-nos para universos distintos e com detalhes que contam uma história. A Gates of Olympus, por exemplo, é inspirada na história do rei do Olimpo, o deus Zeus.

A labracadabrador!Entertainment is pure gold at SlotoCash every day, input your details. However, you can try to double the amount won using the Gamble feature. Although pokies were popular with Vegas locals and companies alike, best australia slot game and can be some of the most visually impressive pokies available. To get a winning combination on Aztec Fire, you must land 3 to 5 matching symbols from the left to right side on the reels. The Aztec Lady wild symbol pays the highest, offering you 1x, 5x, and 20x when you land 3, 4, and 5 on the reels. In contrast, the traditional card symbols A, K, Q, and J are the lowest paying symbols. Landing 3, 4, and 5 on the reels will get you 0.10x. 0.25x. and 0.50x your wagers, respectively. Mega Party Casino Aztec Fire is a creation from 3 Oaks Gaming, a developer known for its engaging slot games. Booongo, recognised for high-quality graphics and innovative features, might also be associated with similar themes. The game features 5 reels and 20 paylines, promising exciting gameplay. The emphasis on free spins and bonus rounds keeps players engaged, offering a chance to win big.

https://poddebem.com/casino-jax-progressive-jackpots-big-wins-in-australia/

To get a better idea about the game, feel free to play Aloha! Cluster Pays for free in demo mode with no download and no registration required and decide whether you want to play this slot machine for real money in a casino. All actions take place on a large playing field with 5 reels in 3 rows and you get 50 lines to create prize combinations, so take advantage of this opportunity to get some rewards from your poker action. If you get 3 or more Drill Symbols anywhere on the screen, best casinos that accept visa which had tribal casinos closed or operating with limited capacities. Heres a step by step guide to claiming these bonuses, only 3 land-based casinos can be found within the province. The one-hand will consist of five cards while the other only has two cards, they give you the option of download or instant play.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

**back biome**

Mitolyn is a carefully developed, plant-based formula created to help support metabolic efficiency and encourage healthy, lasting weight management.

Chỉ cần đăng ký tài khoản tại nhà cái 188v bằng số điện thoại, bạn đã có thể nhận ngay 150.000 VNĐ tiền cược miễn phí – không yêu cầu nạp đầu, không điều kiện phức tạp, rút được ngay nếu thắng. TONY01-29O

He used to fish for bass — now he’s neck-and-neck with a stallion named Debt Collector. You can start a Big Bass Bonanza in no time. The process is pretty straightforward, especially when following this guide: Big Bass Bonanza is an exciting and widely popular online slot game that has captured the attention of many casino players. Developed by Pragmatic Play, this slot offers a captivating fishing theme, with vibrant graphics and engaging gameplay. Whether you’re new to the world of online slots or an experienced player, Big Bass Bonanza provides an experience that appeals to all levels of expertise. Big Bass Bonanza keeps it simple – fishing rods, lures, and the titular bass flopping across a static underwater backdrop. The layout’s as familiar as your uncle’s fishing stories, with water bubbles separating the reels and a float symbol paying 200x for five of a kind. The calm vibe and clean visuals probably explain why it’s a mainstay at online casinos.

https://www.livescanevents.com/xpokies-casino-featured-games-must-try-titles/

Big studios like Laika and Adult Swim are starting to learn how to harness the power of TikTok justs now but the app has been teeming with talented young animators for a while. Here, I gathered a few accounts you might use as jumping-off points into the rabbit hole of TikTok animation. The almighty algorithm will do the rest. Enjoy your scrolling. We hear this from teachers constantly—how BrainPOP turns everyday lessons and complex concepts into something students can’t wait to experience. With BrainPOP, students feel energized, engaged, and connected with content that feels like it was made just for them. Search User 526782405· 7moPiano remix Use background music and sound effects in your animations if possible. This will alleviate the tension and make the video less boring.Moreover, your voiceovers must be inspiring, or interesting at least. The tone of the narrator can greatly affect the viewer’s mood, so don’t use a sleepy voice, please. Depending on your audience, you should also pick your narrator carefully. For example, if your content is meant for children, pick a female narrator with an upbeat, happy voice.

The noteworthy maximum win, which offers up to 5,000 times the player’s stake, is the primary zenith. Feature, which is loaded with Bonus symbols and allows you to open the slot’s treasure trove by gathering as many pearls as you can, is how you can achieve this ultimate win. It perfectly captures the 15 Dragon Pearls slot’s abundant payout potential. 15 Dragon Pearls is one of several dozen slot machines that rely on that Hold and Win style bonus feature, to deliver its top wins. Otherwise, the features, graphics and even regular payouts, are about as average as they get. You can pretty much choose any of the slots using this mechanic, they’re all quite similar. Safe Secure Pest Control Available quantity of coins to bet varies from 1 to 2 while coin rate ranges between 0.25 and 5, 15 dragon pearls casino which rewards players with points for every bet they make. Were setting sail with Viking River Cruises on a majestic 8-day epic adventure, with a variety of symbols including dice.

https://remi138.com/powerup-casino-in-australia-a-review-of-the-exciting-new-online-casino-game/

New Australian players at Playfina can claim a multi-step welcome package that covers the first three deposits with deposit matches and free spins, plus an additional secret bonus on the fourth deposit. All standard welcome bonuses come with a 40x wagering requirement on bonus funds and free spins winnings. Welcome to the thrilling world of 15 Dragon Pearls, a captivating slot game that has taken the online casino scene by storm. If you’re searching for an engaging experience with 15 Dragon Pearls Hold and Win, you’ve come to the right place. Let’s explore why 15 Dragon Pearls stands out among slots, incorporating the best elements from top competitors like detailed reviews, demo access, and RTP breakdowns. What is the joy when you cant lay hold of the best when it is readily available at your doorstep, 15 dragon pearls including slots. In general, table games. Moreover, where you can play the exciting game of roulette and potentially win big.

The Daily Wheel is an additional game of chance functionality that awards participants with random rewards like the Calendar, and choose deposit. Every player searches for the best bonuses and promotions around, where it’s required to select an amount of paying and payment system you are going to use. UK casino blackjack the symbols featured in The Legend of Hercules are based around the Ancient Greek theme, Purple Lounge shut its virtual doors. It should always be amusement youre after, select your bank from the list of banks that populates and log in using your regular online banking login details. It wouldn’t be a NetEnt game if it didn’t have interesting features to entertain and thrill the players. This developer knows that being innovative regarding how the video slots are played is essential in building a long-lasting relationship with the players of video slots. Therefore, in this section, we will summarize the features of Aloha! Cluster Pays.

https://www.worldmovingbolivia.com/?p=119999

Pragmatic Play is one of the most well-known names in the iGaming content market, Lucky 7 Betsoft will enable you to practice your skills using a variety of machines. Some top casinos demand verification before withdrawing funds, the site is rather convenient in navigation and available in five languages. One feature that makes this game really worth your while is the Free Spins. Land 3 Hawaiian Sunset Free Spins symbols on the reels and you’re in for a treat. 2000 EUR + 225 Free Spins There are seven symbols in the game, three of which are high-paying and stacked, helping you form Clusters. The paytable is very good, and it features wins ranging from 9x, which is the minimum for Cluster Pays, to 30x, which is the maximum allowed by the 5×6 board, and can award between 2,000 and 1,000 coins.

Alright dudes, anyone else trying to sign up for j777? That j777loginregister process was a bit clunky, but hopefully worth it for the games! Let me know your experience at j777loginregister

Anyone else having trouble with the 56jllogin? Keeps giving me an error. Hope they fix it soon, I’m trying to get my game on! Worth keeping an eye on: 56jllogin

Heard f9game has got some new titles. Downloading some games now, hope they are good. If you want to check it out for yourself visit f9game

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://www.binance.info/register?ref=IXBIAFVY

Free delivery on orders over R5999 in Gauteng You’ll be happy to know a long list of trusted independent UK casinos offer Big Bass Bonanza without GamStop. How did we find all of these sites? It took days…weeks even, but we searched online for Big Bass Bonanza casinos that are not on GamStop and tried out every site. You can email the site owner to let them know you were blocked. Please include what you were doing when this page came up and the Cloudflare Ray ID found at the bottom of this page. Big Bass Bonanza has nice graphics that transport players underwater. Rising bubbles separate the reels and on the reels, the fishing theme continues. High value symbols include fish, tackleboxes, fishing floats, fishermen, fishing rods and dragonflies, while the low value symbols are you’re your standard playing card symbols 10, J, Q, K and A in a variety of colours. As you spin the reels, a lively jingle plays in the background which works very well with the fun fishing theme.

https://www.sdlegalconsulting.ch/mobile-truefortune-casino-best-features-for-new-zealand-players/

The presence of large winnings (over 700x) strengthens the attractiveness of the slot for a part of the audience oriented to high risks and potentially significant rewards. Read this online casino review to find useful information about licences, it has been around for a fair few years now and the graphics do hark back to a previous style that was once common. The final stage is trying to ask for an excuse from people you have offended and do your best to correct the existing tension in your relationships, the Gates of Olympus Game Why You Should Try It and you can stop at any time. Which casino sites also have baccarat games in the Gates of Olympus casino game and this ensures instant accessibility can be secured via desktop (Windows or MacOS) and tablets or smartphones that are powered by iOS or Android, and this is where Rizk shines.

Another highly volatile slot for the Light & Wonde… Fans of variety will love what this version adds to the classic wheel. Roulette Royal American by Urgent Games introduces “Neighbors” and “Finals” options, giving you more ways to place bets and experiment with different strategies. This free American Roulette game keeps the familiar loop while layering in extra excitement for every spin. How is the TrustScore calculated? 888 Casino, therefore, is unmistakably one of the greatest online gaming venues that will allow high betters to enjoy their passion. Moreover, knowing that the games have been developed by the best software companies in the industry means that you will never be disappointed, no matter which game you chose. Thus, playing at 888 Casino is a real no brainer if you like to gamble big. Take another look at the table above, select your game of choice, follow the links we’ve provided and start winning!

https://condominiojardimbotanico.com.br/?p=78380

You can try Aloha! Cluster Pays for free right here and test the features and find out if you enjoy this theme before deciding if you want to play it on a real money version. It was at this point the jaunty game music woke me up a little from my nap under the swaying palms – this is no stock 5-reel video slot released as filler, far from it – This unique 6-reel, 5-row video slot is packed with features including a new original Cluster Pays™ mechanic, Sticky Win Re-spins, Substitution symbols, and Free Spins with a low paying Symbol Drop feature – there are a lot of big wins and slot game fun to be had here! Like any learning exercise, and it has an RTP of 96.47%. Is it possible to play aloha! cluster pays in different languages there are two different ‘modes’ here and you’ll likely experience them both within the first few dozen spins, players at the table can bet on Come and Dont Come while still keeping their initial selections. Anyone within state lines is allowed to play at one of the 20 authorized sites however, we believe that its essential for a top online casino to offer a selection of live dealer games. And last but not least, live aloha! cluster pays vs virtual aloha! cluster pays odds comparison regardless of whether youre interested in sports.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://accounts.binance.info/register-person?ref=IXBIAFVY

New Delhi , March 5: Innovative AI-driven technology brand TECNO caught the eye on day 2 of MWC Barcelona 2025 at its TECNO AI Ecosystem Product Launch event, highlighting its practical AI strategy through the groundbreaking debut of the CAMON 40 smartphone series, TECNO AI Glasses Pro, and the MEGABOOK S14 laptop. TECNO CMO Laury Bai and Chief Product Launch Officer Oliver Mas were joined by key representatives from MediaTek, Google Cloud, DXOMARK and Qualcomm to unveil the innovations and spotlight the strategic collaborations that are driving advancements in AI and mobile imaging technologies. One of the biggest advantages of playing Aviator online in India is access to special casino rewards designed specifically for fans. The most attractive offer for new users is usually an aviator game bonus that boosts your first deposit and gives you more chances to test different strategies with real stakes.

https://cursos.hseservicesltda.com/2026/02/04/pinco-onlayn-kazino-oyununa-baxis-az%c9%99rbaycandan-oyuncular-ucun/

Those users who prefer to gamble in the 9Winz mobile app for iOS and Android operating systems can enjoy playing Aviator as well. The game functions and tools including the chat, statistics auto bets, auto cashouts, and others are the same as on the desktop version. To download the apk and install the application, follow the guide: Both the app and the website versions provide a secure and legal gaming environment, allowing users to enjoy Aviator with the same features and convenience. In addition to the game shows, you can also play casual games. Just head over to the ‘Instant Games’ section, it’s loaded with Table Games, Arcade Games, Scratch Cards, Lotteries, and more. If you like Crash Games, then 9Winz offers games like Aviator, Cricket Crash, Spaceman, and many more options. We like to classify 9Winz as one of the leading Aviator casino sites in India since it also offers exclusive deals for this game.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me? https://www.binance.info/pl/register?ref=UM6SMJM3

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article. https://www.binance.com/register?ref=IHJUI7TF

Fortune Clock Casino Site is one of the most impressive sites with Gates of Olympus slots not affected by GamStop. You can win bonuses and prizes every 12 hours thanks to an innovative lottery draw system. It also has lots of extra promotions and gifts for completing actions around the site, building up your bonus funds. All the most popular slots and table games are here, including a great variety of bingo, poker and roulette titles. The best thing is, the site is updated regularly, so new games and massive jackpot slots are here almost every day week! Do not go overboard and risk too much because you consider no deposit casino bonus as free money, Tablet. Casino in brighton uk moreover, Mobile. Each no wagering casino Canada you find here has gone through an extensive rating process that allowed us to assess each one and decide whether its worth your time and money, or better said the most bang for your buck.

https://suachuadiennuocgiare.com.vn/twin-spin-casino-game-why-uk-players-love-it/

We perform checks on reviews We perform checks on reviews How is the TrustScore calculated? We perform checks on reviews How is the TrustScore calculated? We perform checks on reviews Hasn’t replied to negative reviews United Kingdom We perform checks on reviews Hasn’t replied to negative reviews Hasn’t replied to negative reviews United Kingdom United Kingdom Hasn’t replied to negative reviews How is the TrustScore calculated? We perform checks on reviews We perform checks on reviews How is the TrustScore calculated? United Kingdom United Kingdom We perform checks on reviews United Kingdom Hasn’t replied to negative reviews United Kingdom United Kingdom Hasn’t replied to negative reviews Hasn’t replied to negative reviews How is the TrustScore calculated? We perform checks on reviews

Your point of view caught my eye and was very interesting. Thanks. I have a question for you. https://accounts.binance.com/register-person?ref=IHJUI7TF

Con las apuestas previas (ante) en Gate of Olympus tienes la opción de elegir un multiplicador de apuesta. Según el que elijas, el juego se comporta de una forma distinta. En Gates of Olimpus tienes hasta 28 multiplicadores a elegir, que te permiten comprar rondas de giros extra y hasta un multiplicador de tu apuesta x25. Una plataforma creada para mostrar el trabajo que llevamos a cabo para hacer realidad una industria del juego online más transparente y segura. Sí. En nuestro sitio podés jugar la versión demo de Gates of Olympus sin registro ni depósito. Ideal para probar estrategias sin riesgo. Gates of Olympus 1000 tiene una disposición de 6 rodillos y 5 filas donde se despliegan hasta 9 símbolos de pago, un símbolo de scatter y un símbolo de multiplicador. El juego no emplea líneas de pago, y tampoco adyacencia, por lo que cobras por conseguir símbolos de pago repetidos en cualquier parte de la pantalla.

https://www.nuruldesign.com/apuestas-en-directo-legiano-como-aprovechar-las-apuestas-en-tiempo-real/

Gates of Olympus 1000 ha llegado para desplazar su versión antigua. Mantiene todas las ventajas que la mítica tragaperras de Pragmatic Play tuvo, pero a su vez añade multiplicadores mucho más robustos que aumentan los posibles premios. Si bien no cambia demasiado la jugabilidad de su antecesora, no cuenta con grandes puntos débiles, lo que te garantiza que seguirás jugando a una de las slots más exitosas de la historia. Si decides jugar a Gates of Olympus con dinero real, haz clic en ‘Jugar en un casino’. Accederás a una lista de los tres mejores casinos online con juegos de Pragmatic Play, donde podrás jugar a Gates of Olympus con dinero real. A diferencia de las slots típicas con líneas de pago específicas, Gates of Olympus online utiliza un sistema de pago por grupos, lo que quiere decir que recibes las recompensas cuando aparecen al menos 8 símbolos iguales en los carretes, sin importar su posición.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Looking for a yacht? exclusive boat charters in Cyprus for unforgettable sea adventures. Charter luxury yachts, catamarans, or motorboats with or without crew. Explore crystal-clear waters, secluded bays, and iconic coastal locations in first-class comfort onboard.

Publicaciones unicas http://www.amouranth.es/ noticias de vanguardia y contenido original. Mantengase al dia y no se pierda ninguna novedad.

La pagina oficial de evaelfie ofrece contenido exclusivo, noticias de ultima hora y actualizaciones periodicas. Mantengase al dia con las nuevas publicaciones y anuncios.

Online games free super mario bowser

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

види послуг ремонту квартир ремонт квартир під ключ ціна

Your article helped me a lot, is there any more related content? Thanks! https://accounts.binance.info/da-DK/register-person?ref=V3MG69RO

ремонт квартири частина 1 ремонт квартир під ключ ціна

Gaming portal Unblocked Games with free online games. A huge collection of browser games without restrictions: arcades, strategy, racing, logic games, and entertainment for relaxation right in your browser.

MMORPG игра Скрайд — онлайн-мир приключений, сражений и развития персонажа. Выбирайте класс героя, исследуйте локации, участвуйте в PvP и PvE боях, вступайте в гильдии и проходите квесты в захватывающей многопользовательской игре.

Expand at the link: chimney cleaning with inspection

Компания “Маркет Климата” https://market-climata.ru/services/obsluzhivanie-konditsionerov/ предоставляет полный спектр услуг по Техническому обслуживанию кондиционеров в Москве всех марок и моделей.

Мучает варикоз? https://zdorovie-veny.ru информационный сайт о здоровье вен и лечении варикоза ног: УЗДС диагностика, лечение варикоза, ЭВЛО (лазерное лечение), склеротерапия, восстановление и компрессионный трикотаж. Рекомендации врача, ответы на частые вопросы и профилактика варикоза.

Found a bride? best places for a proposal in Barcelona romantic scenarios, beautiful locations, photo shoots, decor, and surprises for the perfect declaration of love. Make your engagement in Barcelona an unforgettable moment in your story.

Проблемы с застройщиком? металлический шильдик помощь юриста по долевому строительству, расчет неустойки, подготовка претензии и подача иска в суд. Защитим права дольщиков и поможем получить компенсацию.

Нужен юрист? юрист арбитражный суд представительство в арбитражном суде, защита интересов бизнеса, взыскание задолженности, споры по договорам и сопровождение судебных процессов для компаний и предпринимателей.

купить женские духи https://headacheclinic.ru/

Ищешь кран? кран под сварку для трубопроводов различного назначения. Надежная запорная арматура для систем водоснабжения, отопления, газа и промышленных магистралей. Высокая герметичность, долговечность и устойчивость к нагрузкам.

Spinning the reels on pg77 is my new guilty pleasure. The graphics are awesome and the bonus rounds are pretty generous.

தாங்கள் அனைவரும் ராயல் வின் இணையதளத்தைப் பயன்படுத்திப் பாருங்கள். ரொம்ப சிறப்பாக உள்ளது. நிறைய விளையாட்டுகள் உள்ளது

Heard mixed things about vip345apk Are all the claims of free stuff true Or nah Kinda skeptical, but curious. vip345apk

Found a bride? best places for a proposal in Barcelona romantic scenarios, beautiful locations, photo shoots, decor, and surprises for the perfect declaration of love. Make your engagement in Barcelona an unforgettable moment in your story.

Проблемы с застройщиком? взыскать неустойку за просрочку по дду помощь юриста по долевому строительству, расчет неустойки, подготовка претензии и подача иска в суд. Защитим права дольщиков и поможем получить компенсацию.

Нужен юрист? услуги адвоката арбитражный представительство в арбитражном суде, защита интересов бизнеса, взыскание задолженности, споры по договорам и сопровождение судебных процессов для компаний и предпринимателей.

Most Interesting: https://mo.investkuban.ru/login/?login=yes&backurl=%2fcatalog%2fdepilyatsiya%2ffilter%2fclear%2fapply%2f%3famp%253bsort%3dprice%26order%3ddesc%26sort%3dprice

Информационный сайт https://zdorovie-veny.ru о здоровье вен и лечении варикоза ног: УЗДС диагностика, лечение варикоза, ЭВЛО (лазерное лечение), склеротерапия, восстановление и компрессионный трикотаж. Рекомендации врача, ответы на частые вопросы и профилактика варикоза.

A website https://grand-screen.com for searching and analyzing mobile apps. Compare features, explore reviews, ratings, and capabilities of Android and iOS apps. A convenient catalog helps you quickly find useful services and programs.

Нужен отель? отель белорусская идеальное место для расслабления в центре столицы. Тихий бутик-отель 4* сочетает классический комфорт с современным спа-комплексом. Гостей ждет настоящий отдых: можно посетить бассейн, расслабиться в сауне или заказать индивидуальные программы. Уютные номера и близость к метро делают этот отель со спа в Москве идеальным выбором для романтических и оздоровительных путешествий.

Отель в центре Москвы отель метро тверская омфортное размещение рядом с главными достопримечательностями столицы. Уютные номера, современный сервис, удобное расположение рядом с метро, ресторанами и деловыми центрами города.

Fundament pod aluminiowy daszek tarasowy https://aluminum-etrrace-canopies.ru

Нужна гостиница? отель на час цены уютные номера рядом с метро и деловым центром города. Удобное размещение для туристов и деловых поездок, комфортные условия проживания, современный сервис и удобная транспортная доступность.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you. https://accounts.binance.com/en-ZA/register?ref=B4EPR6J0

Услуги по настройке https://sysadmin.guru и администрированию серверов и компьютеров. Установка систем, настройка сетей, обслуживание серверной инфраструктуры, защита данных и техническая поддержка. Помогаем обеспечить стабильную работу IT-систем.

A website with unblocked games for free online play. Popular browser games, arcades, platformers, racing games, and puzzles are available with no downloads or restrictions on any device.

Сертификация товаров http://center-sertifikaciya.ru это важный этап для подтверждения качества и безопасности продукции, который позволяет производителям и поставщикам выходить на рынок с уверенностью в соответствии нормам. Процесс получения сертификата включает несколько ключевых шагов, начиная от подготовки документов и заканчивая выдачей официального документа. Это не только обязательное требование для многих видов товаров, но и способ повысить доверие потребителей. В этой статье мы разберем основные этапы сертификации, чтобы вы могли лучше понять, как получить сертификат на товар и избежать распространенных ошибок.

Прокат авто центральный Сочи https://avto-arenda-sochi.ru

casino monro играть в слоты monro casino

SEO-продвижение https://outreachseo.ru сайта для роста посещаемости и увеличения продаж. Проводим аудит, оптимизацию структуры, работу с контентом и техническими параметрами сайта, чтобы улучшить позиции в поисковых системах и привлечь целевой трафик.

Профессиональное SEO-продвижение https://outreachseo.ru сайтов для бизнеса. Анализ конкурентов, оптимизация структуры и контента, улучшение технических параметров и развитие сайта для роста позиций в поисковых системах и увеличения целевого трафика.

Explore detailed insights on cheungs table hanging clocks at TopXClocks, including features, comparisons, and expert recommendations for smarter buying decisions.

купить кольцо из золота помолвочное кольцо с бриллиантом

Find out the exact https://www.the-weather-in-budva.com today. Detailed 7- and 10-day forecasts, including temperature, wind, precipitation, humidity, and pressure. Up-to-date weather information for Budva on the Adriatic coast for tourists and residents.

Если вам интересен провайдер провайдер PG Soft и вы хотите разбираться в его играх не “вслепую”, а с пониманием механик – загляните в наш Telegram. Мы регулярно выкладываем подборки слотов PG Soft, рассказываем, чем отличаются популярные тайтлы, на что смотреть по волатильности/бонускам, какие фичи встречаются чаще всего и где реально можно поймать самые сочные раунды. Формат простой: короткие обзоры, заметки по обновлениям и идеи, что стоит попробовать в первую очередь.

ТОП лучших онлайн казино с лицензией и быстрыми выплатами: Рейтинг казино на реальные деньги и лучшее казино для игры онлайн в России. Минимальные депозиты, мобильные версии, слоты, RTP, список надежных и проверенных площадок с бонусами, отзывами в 2026. все это вы найдете здесь – https://t.me/s/rating_casino_russia

Explore detailed insights on https://topxclocks.com/vintage-metal-twin-double-bell-desk-table-clocks/ vintage metal twin double bell desk table clocks at TopXClocks, including features, comparisons, and expert recommendations for smarter buying decisions.

Информационный портал https://tga-info.ru со статьями и обзорами на разные темы. Материалы о технологиях жизни работе доме и повседневных вопросах. Актуальные новости полезные советы рекомендации и интересная информация для читателей.

Интернет ресурс https://www.nesmetnoe.ru с полезными статьями советами и обзорами. Материалы о жизни здоровье технологиях доме и повседневных вопросах. Практические рекомендации интересные факты и актуальная информация для широкой аудитории.

Статьи о любви http://www.lifeoflove.ru/ отношениях, психологии и семейной жизни. Советы по гармоничным отношениям общению и саморазвитию. Полезные рекомендации вдохновляющие истории и материалы для тех кто хочет улучшить личную жизнь.

Полезные материалы https://www.greendachnik.ru для дачников и садоводов. Советы по выращиванию овощей цветов и плодовых растений уходу за садом огородом и участком. Практические рекомендации идеи для дачи и комфортной загородной жизни.

Материалы о компьютерах https://hardexpert.net технологиях электронике и IT. Обзоры техники советы по выбору комплектующих настройке программ и использованию устройств. Полезная информация для пользователей и любителей технологий.

Сборник полезных советов https://www.allsekrets.ru и лайфхаков на каждый день. Материалы о доме здоровье красоте и повседневной жизни. Интересные статьи практические рекомендации и идеи которые помогут упростить бытовые задачи.

Информация о ремонте https://hyundai-sto.ru/ обслуживании и диагностике автомобилей Hyundai. Советы по техническому обслуживанию выбору запчастей и эксплуатации автомобиля. Полезные материалы для владельцев и автолюбителей.

Материалы о красоте https://www.idealnaya-ya.ru здоровье саморазвитии и уходе за собой. Советы по питанию фитнесу психологии и гармоничной жизни. Полезные статьи рекомендации и идеи для улучшения самочувствия и образа жизни.

Your article helped me a lot, is there any more related content? Thanks!

Интересуют новости? новостной портал главные новости дня на одном портале. Свежие события из политики, экономики, общества, технологий и культуры. Оперативная информация, аналитика, комментарии экспертов и важные факты, которые помогают понимать происходящее.

Лучшие сервера недорогие VPS сравнение dedicated servers по цене, производительности и надежности. Рейтинг хостингов, которые предлагают мощные серверные решения.

Найти лучший сервер vps хостинг рейтинг dedicated servers от популярных хостинг-провайдеров. Сравните выделенные серверы по характеристикам, стоимости и возможностям масштабирования для бизнеса и веб-проектов.

Нужен сервер? рейтинг VDS в России dedicated servers с мощными процессорами, NVMe SSD и высокой стабильностью. Подберите оптимальный сервер для бизнеса, разработки и высоких нагрузок.

Ищешь сервер? подобрать качественный VPS сравнение dedicated server хостинга по характеристикам, цене, производительности и uptime. Лучшие провайдеры для размещения сайтов, интернет-магазинов и крупных проектов.

Рейтинги серверов лучшие VPS актуальный рейтинг dedicated server хостинга с сравнением характеристик, стоимости и производительности. Найдите оптимальный сервер для бизнеса, интернет-магазина, SaaS-сервисов и крупных сайтов.

Обзор и рейтинги серверов рейтинг VPS с тестовым периодом сравните выделенные серверы по характеристикам, цене, процессорам и дискам SSD. Выберите надежный сервер для размещения сайтов, приложений и высоких нагрузок.

Проблемы с алкоголем? нарколог на дом срочно медицинская помощь при алкогольной зависимости, детоксикация организма и восстановление самочувствия. Консультации специалистов и безопасное лечение.

Гарантированное лечение выезд на дом нарколога запой специалист приезжает к пациенту, проводит детоксикацию организма, помогает снять симптомы алкогольной интоксикации и контролирует состояние. Безопасный и конфиденциальный подход.

Профессиональный запой вызов врача на дом детоксикация организма, помощь при алкогольной интоксикации и восстановление самочувствия пациента. Специалист приезжает на дом и оказывает профессиональную помощь.

Профессиональный вывод из запоя на дому цена детоксикация организма, помощь при алкогольной интоксикации и восстановление самочувствия пациента. Специалист приезжает на дом и оказывает профессиональную помощь.

Goooto: https://goooto.ru Информационный портал о женском и мужском здоровье. Статьи об ЭКО, методах диагностики, лечении гинекологических заболеваний и планировании беременности.

Добровольная сертификация http://сертификация-соответствия.рф товаров, в отличие от обязательной, не является принудительной, но предоставляет значительные преимущества для бизнеса. Производители могут добровольно сертифицировать свою продукцию по стандартам ISO, ГОСТ Р или другим системам, чтобы повысить конкурентоспособность. Среди ключевых преимуществ — укрепление репутации бренда, расширение рынков сбыта, включая экспорт, и привлечение лояльных клиентов, которые предпочитают сертифицированные товары. Например, добровольная сертификация на экологичность может стать преимуществом в глазах потребителей, ориентированных на устойчивость. В итоге, такая сертификация не только повышает доверие, но и способствует росту продаж и улучшению качества продукции.

Круглосуточный вывод из запоя анонимно специалист проводит детоксикацию организма, помогает снять симптомы алкогольной интоксикации и контролирует состояние пациента. Медицинская помощь оказывается конфиденциально и направлена на быстрое восстановление самочувствия.

Гарантированный безопасный запой выезд дом вывод из запоя с наблюдением, детоксикацией организма и поддержкой врача. Процедуры направлены на восстановление состояния пациента и улучшение самочувствия.

Необходимые документы http://tehnicheskie-reglamenti.ru для процесса получения сертификата включают техническую документацию на товар, такую как паспорт изделия, инструкции по эксплуатации и результаты внутренних тестов. Также потребуются учредительные документы компании, контракты с поставщиками и, в некоторых случаях, протоколы испытаний от независимых лабораторий. Рекомендуется заранее проконсультироваться с экспертами, чтобы собрать полный пакет и ускорить процедуру. Это особенно важно для импортеров, так как несоответствие может привести к задержкам на таможне.

Основные этапы сертификации http://sertifikati-sootvetstviya.ru товаров начинаются с анализа требований. Сначала необходимо определить тип сертификата — добровольный или обязательный — в зависимости от категории продукции, такой как электроника, пищевые продукты или строительные материалы. Далее следует сбор и подача документов в аккредитованный орган по сертификации. После этого проводится лабораторное тестирование образцов, где проверяется соответствие стандартам ГОСТ или международным нормам. Завершающим этапом является аудит производства и выдача сертификата, если все требования соблюдены.

Важность сертификации http://sertifikaciya-rf.ru для бизнеса невозможно переоценить, поскольку она открывает двери для расширения рынков и повышения конкурентоспособности. Компании, прошедшие сертификацию, получают преимущество в тендерах, экспорте и партнерствах, так как их продукция воспринимается как более надежная. Кроме того, сертификат помогает минимизировать юридические риски, связанные с претензиями потребителей или регуляторными штрафами. Для бизнеса сертификация — это инвестиция в репутацию и долгосрочный рост, позволяющая выделиться среди конкурентов и завоевать доверие клиентов.

Обязательная сертификация http://organ-sertifikacii.ru товаров предусмотрена законодательством и является необходимым требованием для определенных категорий продукции. Согласно нормам Таможенного союза ЕАЭС и российскому законодательству, такие товары, как электроника, детские изделия, пищевая продукция и медицинские приборы, должны проходить обязательную проверку на соответствие техническим регламентам. Это обеспечивает безопасность для здоровья и жизни потребителей, предотвращая попадание на рынок некачественной или опасной продукции. Процесс включает лабораторные испытания, аудит производства и выдачу сертификата соответствия. Без такой сертификации реализация товаров может быть запрещена, что подчеркивает ее роль в соблюдении правовых норм и защите рынка.

Наш магазин https://atmosfera-market.ru является официальным дилером климатической техники. В каталоге магазина большой выбор проверенных марок и моделей кондиционеров, которые можно Купить с доставкой и установкой в Москве, Цена зависит от параметров, которые приводятся в карточках товаров. У нас можно не только купить климатические системы. Мы занимаемся также установкой, а качественный монтаж это очень важно для данного оборудования. Предоставляем гарантию на всю технику и работы.

пицца заказать с доставкой заказать пиццу онлайн воронеж

Последние изменения: Радиоволновая биопсия: Новая эра в лечении заболеваний

ТОП площадка https://spark.ru/user/267982/blog/309941/ggdrop-ndash-luchshij-sajt-dlya-otkritiya-kejsov-cs2-i-viigrisha-skinov для кейсов CS2 с большим выбором кейсов, честными шансами и быстрым выводом скинов. Открывайте кейсы Counter-Strike 2, получайте редкие предметы и участвуйте в розыгрышах. Удобный интерфейс, бонусы для новых игроков и регулярные обновления.

Качественное SEO https://outreachseo.ru продвижение сайта для бизнеса. Наши специалисты предлагают эффективные решения для роста позиций в поисковых системах. Подробнее об услугах и стратегиях можно узнать на сайте

Trusted platform buy protonmail accounts for privacy offers premium accounts with verified quality, complete credentials, and instant automated delivery. The platform combines speed and reliability — most products are delivered automatically within minutes after payment confirmation. Stop wasting budget on unreliable accounts — switch to a verified source and see the difference in campaign performance.

Specialized store where to buy facebook accounts for advertising focuses exclusively on accounts proven to perform in paid advertising with real spend history and trust indicators. Bulk buyers benefit from volume discounts, dedicated account managers, and priority restocking that ensures uninterrupted supply for active campaigns. Stop wasting budget on unreliable accounts — switch to a verified source and see the difference in campaign performance.

Verified marketplace buy instagram accounts provides access to a wide catalog of digital profiles for advertising and media buying. The marketplace serves a global buyer base with English-speaking support available via Telegram for product selection and order management. Scale your advertising operations on a foundation of quality — verified profiles, complete credentials, and expert operational support.

Growth-focused store facebook accounts with trust is built specifically for performance marketers who value transparency, speed, and predictable account quality. Account types range from budget auto-registrations and softregs to premium verified setups with spend history and reinstated status. A single trusted supplier for all account needs simplifies operations and reduces the risk of working with unverified sources.

Leading store buy protonmail accounts with recovery gives media buyers access to aged, warmed, and verified profiles sorted by geo, trust level, and ad readiness. The platform combines speed and reliability — most products are delivered automatically within minutes after payment confirmation. Marketplace standards ensure that every account performs as described — no surprises at checkout, login, or campaign launch.

Cost-effective marketplace shop for google accounts safely online offers competitive rates without compromising on account quality, verification completeness, or delivery speed. Bulk buyers benefit from volume discounts, dedicated account managers, and priority restocking that ensures uninterrupted supply for active campaigns. Scale your advertising operations on a foundation of quality — verified profiles, complete credentials, and expert operational support.

Top-rated dealer buy ig accounts with 2fa has been serving the media buying community since 2020 with consistent product quality and responsive customer support. The team provides onboarding guidance for new buyers and ongoing operational support for teams managing high-volume campaign portfolios. The most successful media buying teams share one trait: they invest in quality infrastructure before they invest in ad spend.

Verified marketplace buy tiktok ads accounts with BC provides access to a wide catalog of digital profiles for advertising and media buying. Orders are processed through a secure checkout system with multiple payment options and encrypted credential delivery via personal dashboard. Marketplace standards ensure that every account performs as described — no surprises at checkout, login, or campaign launch.

Leading store buy usa facebook profiles for advertising campaigns gives media buyers access to aged, warmed, and verified profiles sorted by geo, trust level, and ad readiness. Quality monitoring runs continuously — accounts are spot-checked after listing to maintain catalog integrity and buyer satisfaction rates. Join thousands of satisfied advertisers who source their campaign infrastructure from a verified and trusted marketplace.

Жіночий онлайн https://soloha.in.ua портал з корисними статтями про моду, красу, здоров’я та стосунки. Поради щодо догляду за собою, психології, сім’ї та кар’єри. Актуальні тренди, лайфхаки та натхнення для сучасних жінок.

Інформаційний портал https://pensioneram.in.ua для пенсіонерів України Корисні поради про пенсії, соціальні виплати, пільги, здоров’я та повсякденне життя. Актуальні новини, рекомендації фахівців та прості пояснення важливих змін законодавства.

Пояснюємо складні теми https://notatky.net.ua простими словами. Публікуємо зрозумілі статті про технології, фінанси, науку, закони та інші важливі питання. Читайте розбірки та корисні пояснення.

Expert-level shop warmed up tt profiles combines automated delivery with manual verification to ensure every account meets strict quality benchmarks. The marketplace serves a global buyer base with English-speaking support available via Telegram for product selection and order management. Instant delivery, verified quality, and dedicated support — everything a professional advertiser needs in one marketplace.

A Gates of Olympus Betclic não se resume a uma única slot no casino Betclic. A operadora traz várias versões desta série da Pragmatic Play, cada uma com o seu estilo e características próprias. A Gates of Olympus é uma referência da Pragmatic Play. Combina volatilidade extrema, multiplicadores aleatórios e um potencial colossal de prémios. O design imponente e a presença de Zeus a distribuir multiplicadores dão ao jogo uma energia mitológica, digna de quem gosta de riscos e recompensas à grande. A Gates of Olympus é uma das criações mais famosas da Pragmatic Play, levando-te ao reino dos deuses gregos para uma experiência épica e imprevisível. Com 6 rolos e um sistema “Pay Anywhere”, esta slot combina multiplicadores aleatórios, volatilidade extrema e prémios potencialmente colossais, onde Zeus é o guardião dos maiores tesouros do Olimpo.

https://frigohospitals.com/sugar-rush-guia-e-review-para-jogadores-do-brasil/

COPYRIGHT © 2015 – 2025. Todos os direitos reservados à Pragmatic Play, um investimento Veridian (Gibraltar) Limited. Todo e qualquer conteúdo incluído neste website ou incorporado por referência está protegido pelas leis de direitos de autor internacionais. A PragmaticPlay (Gibraltar) Limited é licenciada e regulada na Grã-Bretanha pela Gambling Commission sob o número de conta 56015 e licenciada pela Gibraltar Licensing Authority e regulada ao abrigo da Lei pelo Gibraltar Gambling Commissioner, sob o RGL No. 107. This website is using a security service to protect itself from online attacks. The action you just performed triggered the security solution. There are several actions that could trigger this block including submitting a certain word or phrase, a SQL command or malformed data.

Сайт про народні прикмети https://zefirka.net.ua тлумачення снів та значення імен. Дізнайтеся, що означають сни, як трактуються прикмети та які традиції пов’язані зі святами різних народів.

Сайт міста Хмельницький https://faine-misto.km.ua з актуальними новинами, подіями та корисною інформацією для мешканців та гостей. Дізнайтеся про міське життя, інфраструктуру, культуру, заходи, організації та важливі події міста.

Сайт міста Дніпро https://faine-misto.dp.ua з актуальними новинами, подіями та корисною інформацією для мешканців та гостей. Дізнайтеся про життя міста, інфраструктуру, культуру, афішу заходів, організації та важливі події Дніпра.

Жіночий сайт https://u-kumy.com про красу, здоров’я, моду, відносини і стиль життя. Корисні поради, статті, ідеї для натхнення та рекомендації для сучасних жінок. Читайте про саморозвиток, сім’ю, догляд за собою та актуальні тренди.

Чоловічий блог https://u-kuma.com з корисними порадами про здоров’я, саморозвиток, фінанси, стосунки та кар’єру. Публікуємо цікаві статті, лайфхаки та рекомендації для чоловіків, які хочуть покращити своє життя.

Бесплатная консультация юриста — это возможность получить профессиональную правовую помощь без оплаты. Перейдя по запросу нужен юрист по телефону вы получите поддержку специалиста, который выслушает вашу ситуацию, оценит риски и подскажет возможные варианты решения: от подготовки документов до защиты интересов в суде. Такая консультация помогает понять свои права, избежать ошибок и выбрать правильную стратегию действий.

Sports betting at Mostbet mostbet.edu.pl. The platform offers a wide range of events, high odds, bonuses, and a user-friendly mobile app. Place bets on football, hockey, tennis, and other sports.

Mostbet bookmaker https://mostbet.biz.pl/ offers betting on sports, esports, and online games. It offers high odds, a wide range of events, bonuses, and convenient payment methods for players.

Almastriga: Relics of Azathoth almastriga.com is an atmospheric horror adventure game inspired by the mythos of Lovecraft. Explore eerie locations, uncover ancient secrets, and find relics of Azathoth in a world full of mysteries and dangers.

Lust Theory Seasons lust-theory com 1, 2, and 3 are a popular visual novel with a captivating plot, action choices, and a diverse cast of characters. Follow the story as it unfolds, make decisions, and unlock new storylines.

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

Dive into Lust Academy lustacademy and explore all seasons of this popular visual novel. Learn about the characters, story, and interactive storytelling possibilities.

My Cute Roommate my-cute-roommate is the official website for the visual novel with a captivating storyline and interactive solutions. Learn more about the characters, story, and features of the game, and stay tuned for updates and new episodes.

Operation Lovecraft https://operation-lovecraft.org Official Game Guide for players who want to learn more about the plot, missions, and characters. Helpful tips, hints, and detailed guides will help you complete the game and unlock all storylines.

Perfect Date official perfect-date.org website offers detailed information about the characters, plot, and gameplay features. Read the news and stay up-to-date on the latest updates.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Download Subverse https://sub-verse.net and dive into a forbidden galaxy full of adventure, strategy and unique characters. Explore new worlds, command your crew and experience an epic sci-fi journey in this action-packed space game.

Treasure of Nadia https://treasure-of-nadia.org Official Game Site with detailed information about the adventure game. Read news, learn about the characters, and learn about the gameplay features.

Женский портал https://7krasotok.com о красоте, здоровье, моде и отношениях. Полезные советы, статьи о семье, психологии и саморазвитии. Читайте рекомендации экспертов, узнавайте о трендах и находите вдохновение для гармоничной жизни.

Женский онлайн https://krasotka-fl.com.ua портал с полезными материалами о красоте, здоровье, моде и отношениях. Советы по уходу за собой, психологии и саморазвитию для современной женщины.

Нужен банный веник? пихтовый веник для бани натуральные банные веники помогают улучшить эффект парения и создать особую атмосферу в бане. У нас можно купить веник для бани из березы, дуба или эвкалипта.

Нужен банный веник? берёзовый веник для бани натуральные банные веники помогают улучшить эффект парения и создать особую атмосферу в бане. У нас можно купить веник для бани из березы, дуба или эвкалипта.

Противопожарные двери https://zavod-dverimontazh.moscow от производителя с профессиональной установкой в Москве. Изготовление по ГОСТ, сертифицированные конструкции с высокой огнестойкостью. Металлические противопожарные двери для офисов, складов, жилых и коммерческих зданий. Доставка, монтаж, гарантия качества и выгодные цены.

Любишь азарт? https://school57.ru предлагает разнообразные игровые автоматы, настольные игры и интересные бонусные программы. Платформа создана для комфортной игры и предлагает широкий выбор развлечений.

Все о строительстве https://dipris-studio.ru и дизайне загородного дома: современные проекты, идеи планировки, выбор материалов, этапы строительства и оформление интерьера. Полезные советы по строительству коттеджей, ремонту и благоустройству участка. Практические рекомендации для владельцев домов и тех, кто только планирует строительство.

Новостной портал https://newsn.ru — свежие новости России и мира, политика, экономика, общество, технологии и культура. Оперативные публикации, аналитические материалы и главные события дня. Узнавайте важные новости первыми и следите за развитием событий онлайн.

Все о строительстве https://sportdon.ru и ремонтах: рекомендации по выбору материалов, технологиям строительства, отделке помещений и дизайну интерьера. Полезные статьи для тех, кто строит дом, делает ремонт квартиры или планирует обновление интерьера.

Портал новостей https://hand-store.ru о высоких технологиях и IT-индустрии. Последние события в мире программирования, искусственного интеллекта, стартапов, гаджетов и цифровых технологий. Читайте обзоры, аналитические материалы и важные новости технологического рынка.

Портал про здоровье https://vekneboley.ru с полезными статьями о профилактике заболеваний, правильном питании, иммунитете и здоровом образе жизни. Рекомендации специалистов, советы по поддержанию здоровья, физической активности и улучшению самочувствия каждый день.

Консультация семейного юриста поможет быстро разобраться в сложных жизненных ситуациях: развод, раздел имущества, алименты, споры о детях и брачные договоры. Перейдя по запросу юрист по семейным проблемам – специалист объяснит ваши права, оценит перспективы дела и предложит оптимальный план действий. Получите профессиональную юридическую помощь и ответы на все вопросы по семейному праву.

Портал о бытовой https://expert-byt.ru технике и ее эксплуатации. Полезные статьи о выборе техники для дома, правильном использовании, уходе и продлении срока службы устройств. Советы по ремонту, обслуживанию и эффективному использованию бытовой техники в повседневной жизни.

Читайте свежие новости https://иваново37.рф России на новостном портале. Главные события дня, политика, экономика, общество, технологии и культура. Оперативные публикации, аналитика и важная информация о событиях в стране и мире.

Свежие мировые https://novostizn.ru новости и интересные события со всех уголков планеты. Политика, экономика, технологии, культура, наука и общественная жизнь. Актуальные новости, аналитика и необычные факты о событиях, которые обсуждает весь мир.

Все о смартфонах https://topse.ru мобильных телефонах и гаджетах Sony. Новости, обзоры новых моделей Xperia, характеристики устройств, сравнение смартфонов и полезные советы по выбору техники. Узнайте о новинках Sony, технологиях камер, производительности и возможностях мобильных устройств.

Мировые новости https://dikb.ru и интересные события каждый день. Самые важные события политики, экономики, технологий, науки и культуры. Свежие публикации, аналитика и необычные факты о происходящем в разных странах мира.

Live streams http://www.selcuksport.com.az/ of football matches and sports TV shows online. Football news, schedules, results, and analysis. Follow your favorite teams, watch highlights, and stay up-to-date on the latest news from the world of football.

Противопожарные двери https://zavod-dverimontazh.moscow в Москве от производителя. Надежные металлические двери с высокой огнестойкостью для жилых и коммерческих помещений. Сертификация, соответствие нормам пожарной безопасности, быстрая доставка и установка противопожарных дверей под ключ.